Charitable Giving Made Easy

Stifel clients often seek ways to meet their philanthropic goals while maximizing tax benefits. There are a variety of charitable giving strategies available, including donor-advised funds, pooled income funds, charitable remainder trusts, and private foundations. Although they all provide both income tax and estate tax benefits, each of these strategies is unique.

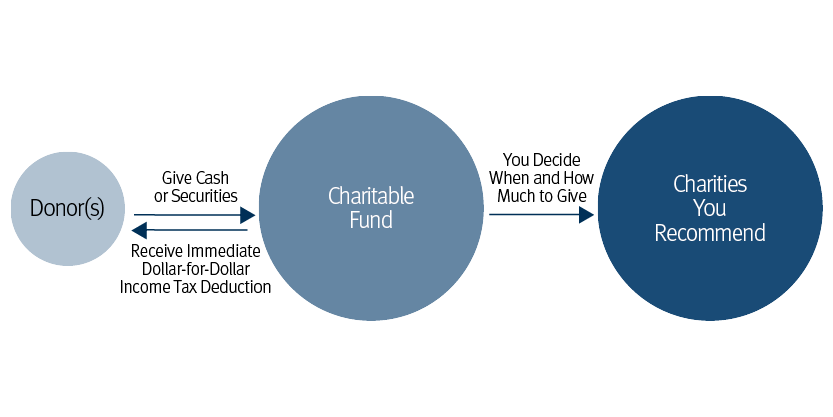

Donor-Advised Funds

A donor-advised fund (DAF) is a fund created and administered by a charitable organization to which donors contribute assets. Each donor’s contributions are held in a separate account earmarked for charitable giving. Over time, the donor can recommend distributions be made to an individual charity or charities.

Over the past several years, DAFs have significantly increased in popularity due to their flexibility and overall simplicity. They have no upfront costs or administrative hassle, such as annual tax filings, and they accept a wide range of assets as contributions. Because DAFs handle the administrative burden, they do charge a small administrative fee.

The tax benefits of DAFs also make them very appealing. When a donor contributes assets to a DAF, he or she receives an immediate income tax deduction while decreasing the value of his or her estate for estate tax purposes. Capital gains tax is also avoided on appreciated assets contributed to the DAF.

DAFs are generally appropriate for individuals who want to make charitable gifts using a low-cost strategy that provides administrative convenience and flexibility. Those individuals who benefit most from DAFs are focused on maximizing immediate tax benefits, rather than retaining an income stream from the contributed assets.

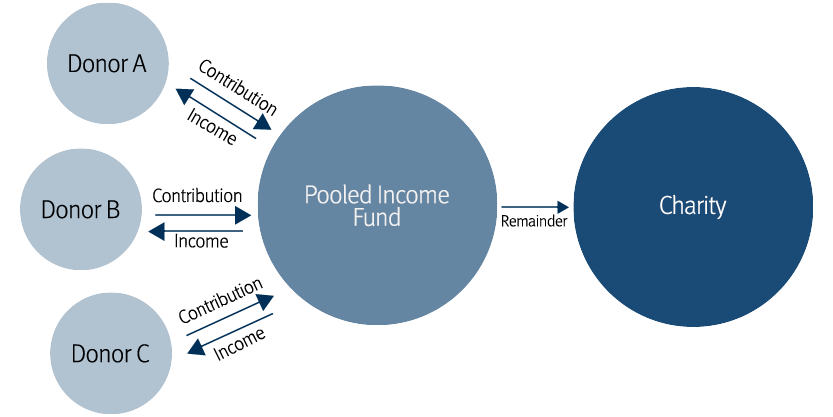

Pooled Income Funds

A pooled income fund (PIF) is a fund created and administered by a charitable organization to which individual donors contribute assets. The property contributed by the donor is commingled with contributions from all other donors and managed as one large pool of assets. The donor will receive income based on the annual performance of the fund. Upon the donor’s death, his or her portion of the fund is distributed to the charity or charities selected by the donor.

PIFs are generally appropriate for a donor who wants to make a charitable gift for the income tax and estate tax benefits, but who also wants to retain an income stream without being subject to the high costs associated with a charitable remainder trust. Individuals who benefit most from a pooled income fund are not focused on maximizing immediate tax benefits, as the income received by the donor reduces the income tax deduction.

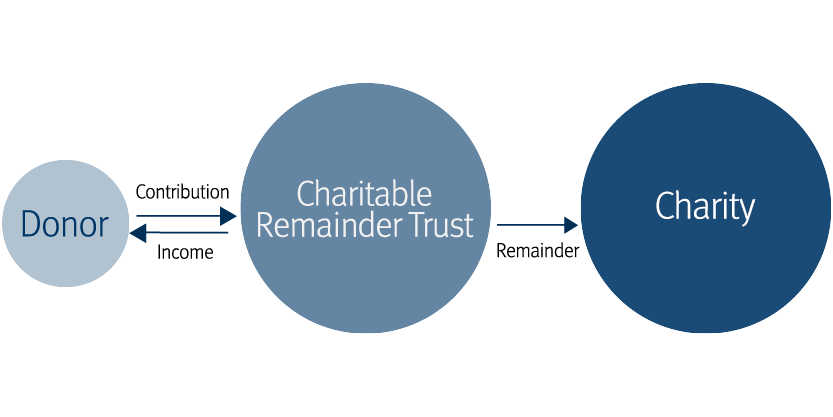

Charitable Remainder Trusts

There are several different types of charitable trusts, all of which involve a contribution of assets to an irrevocable trust created by the donor. The most popular type of charitable trust is called a charitable remainder trust (CRT). The trustee will distribute trust income to the donor for a certain period. At the end of that period, the trustee will distribute the remainder to the charitable beneficiary named in the trust.

CRTs are generally appropriate for a donor who wants to make a charitable gift for the income tax and estate tax benefits, but who also wants to retain an income stream from the assets. Individuals who benefit most from a charitable remainder trust are comfortable with the significant upfront costs to setup the trust and the ongoing administrative burdens caused by annual trust tax filings. Finally, they are not focused on maximizing immediate tax benefits, as the income received by the donor reduces the income tax deduction.

Private Foundations

A private foundation is a legal entity created by an individual or group of individuals for some philanthropic purpose. Although many individuals inquire about private foundations, they are generally most appropriate for individuals with substantial wealth who aim to maximize control while hosting charitable events or paying wages to family member employees. Private foundations are subject to the highest level of IRS scrutiny.When determining which charitable giving strategy is right for you, consider the advantages and disadvantages of the strategies discussed above. The chart below will help provide you with this comparison. If you have any further questions, speak with your Stifel Financial Advisor, attorney, and tax professional.

| DAF | PIF | CRT | Foundation | |

| Upfront Costs | None | None | Professional Fees | Professional Fees |

| Income Stream | None | Yes, this income is taxable | Yes, this income is taxable | None |

| Income Tax Deduction* | Up to 60% of AGI for cash Up to 30% of AGI for appreciated assets |

Up to 60% of AGI for cash Up to 30% of AGI for appreciated assets |

Up to 60% of AGI for cash Up to 30% of AGI for appreciated assets |

Up to 30% of AGI for cash Up to 20% of AGI for appreciated assets |

| Estate Tax Benefits | Assets removed from estate | Assets removed from estate, but income added | Assets removed from estate, but income added | Assets removed from estate |

| Administrative Concerns | Small fees | Small fees | Annual trust tax returns and any associated fees | Annual tax returns, excise taxes, and various others |

* Income tax deductions are limited to a certain percentage of adjusted gross income (AGI) with a five-year carry forward.

Stifel does not provide legal or tax advice. Investors should consult with their professional legal and tax advisors regarding their particular situation.

0122.4178970.1