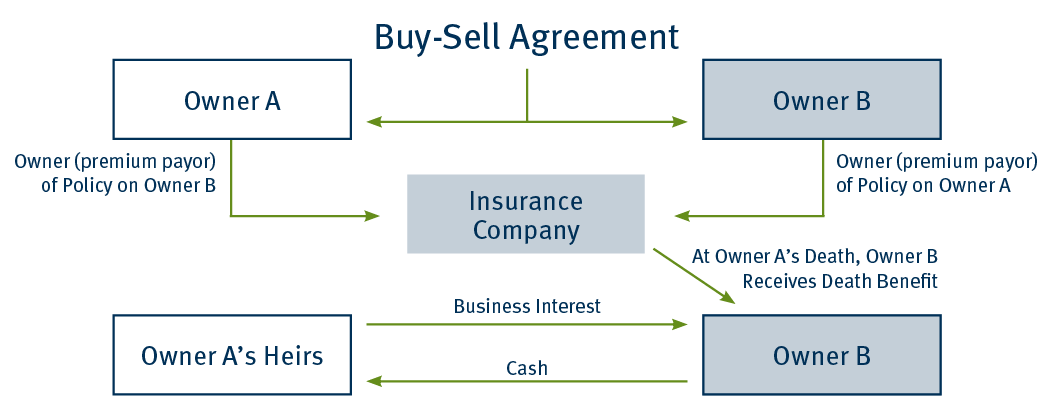

Cross-Purchase Buy-Sell Arrangements

A buy-sell agreement identifies a buyer for a business in the event of an owner’s death. In a cross-purchase arrangement, surviving owners are obligated to purchase the interest of a deceased owner. To fund the buyout, owners purchase life insurance policies on the lives of each of the other owners. Upon an owner’s death, surviving owners receive the death benefit and purchase the deceased owner’s interest from his or her estate. Surviving owners retain control of the business, and the non-liquid business interest is converted to cash for the heirs.

Client Profile

- Business with multiple (typically two) owners

Why It Is Used

- Guarantees a market for future sale of the business

- Guarantees business passes to other current owners

- Provides fair market value for deceased owner’s heirs

- Provides liquidity for the family of a deceased owner

Advantages

- Guarantees a purchaser for the business

- Provides liquidity to meet purchasing obligations

- Surviving owner(s) retain control of the business

- Terms of sale negotiated prior to death

- Heirs of deceased owner receive fair market value

- Family of a deceased owner receives cash to pay estate taxes and/or to meet family needs

- Assurance of continued operation for creditors and employees

Disadvantage

- More owners require more life insurance policies

Role of Life Insurance

- Provides liquidity for surviving owner(s) to meet purchase obligation

- Provides immediate full funding of the purchase price

- Less costly funding method than borrowing the funds or using the company’s working capital

- Leverages premium dollars

Tax Considerations

- Death benefit received income tax free

- Premiums not income tax deductible

- Deceased owner’s estate receives a step-up in basis

- Surviving owner receives step-up in basis on share purchased from deceased owner’s estate

- Not subject to Alternative Minimum Tax (AMT)

IRS CIRCULAR 230 DISCLOSURE: To ensure compliance with the requirements imposed by IRS Circular 230, we inform you that to the extent this communication, including attachments, mentions any federal tax matter, it is not intended or written and cannot be used for the purpose of avoiding Federal Tax penalties. In addition, this communication may not be used by anyone in promoting, marketing, or recommending the transaction or matter addressed herein. Anyone other than the recipient who reads this communication should seek advice based on their particular circumstances from an independent tax advisor. Stifel does not provide legal or tax advice.

0623.5762413.1