Choosing Between Traditional and Roth IRAs

Each year, individuals with earned income may decide to put up to $6,500 ($7,500 if age 50 or older) into an IRA to save for retirement. The decision to contribute to a traditional IRA versus a Roth IRA has several key considerations, such as eligibility, tax deductibility, and current versus future tax rate. The below chart outlines some features of each type of IRA to aid in the important decision of which IRA to fund annually.

| Traditional IRA | Roth IRA | |

| Tax-deductible contributions | Yes1 | No |

| Tax-deferred growth on earnings | Yes | No |

| Tax-free growth on earnings | No | Yes |

| Tax-free distribution of earnings | No | Yes2 |

| Contributions allowed at any age | Yes3 | Yes3 |

| Required minimum distributions (RMDs) at age 72 | Yes | No |

| Contribution eligibility depends on income | No | Yes |

| Contributions may be withdrawn at any time tax-free | No4 | Yes |

1 Dependent on tax filing status, retirement plan coverage, and modified adjusted gross income (MAGI)

2 Five years from first Roth IRA funding and age 59½, first-time home buyer, death, or disability

3 Must have earned income

4 Non-deductible contributions may be withdrawn tax-free, but subject to the pro rata rule

Five important questions to ask

- Do I need a tax deduction, and am I eligible for it?

If you are covered by an employer-sponsored retirement plan and are a single filer, modified adjusted gross income (MAGI) under $73,000 will allow for a full tax deduction on a traditional IRA contribution.

If you are covered by an employer-sponsored retirement plan and are married filing jointly, MAGI under $116,000 will allow for a full tax deduction on a traditional IRA contribution.

If you (and your spouse, if married) are not covered by an employer-sponsored retirement plan, you can have any MAGI level and fully deduct your traditional IRA contribution. - Am I eligible to make a Roth IRA contribution?

If you are a single filer with an MAGI under $138,000, you may make the full $6,500 ($7,500 if age 50 or older) RothIRA contribution.

If married filing jointly with an MAGI under $218,000, you may make the full $6,500 ($7,500 if age 50 or older) Roth IRA contribution. - Is my tax rate going to be higher now or higher in the future?

If you believe your tax rate is going to be the same or higher in the future, a Roth IRA is more beneficial, as those assets will be tax-free after five years and age 59½. - Are my beneficiaries in high tax brackets?

Under the SECURE Act’s 10-year rule, most non-spouse beneficiaries must have inherited IRAs depleted over 10 years, unless the decedent IRA was past RBD. Then, the beneficiary will be taking minimum distributions each year until the tenth anniversary of death.

If beneficiaries are in a high tax bracket, inherited tax-free Roth IRA money does not get taxed at the beneficiary’s high rate. - How long do I have until retirement or needing access to this money?

The younger you are, the longer time horizon you have in which to compound earnings in an IRA.

Since Roth IRA earnings will eventually be tax-free, Roth IRAs become more appealing for younger investors.

Please Note: Withdrawals prior to age 59½ may be subject to taxes and a 10% penalty.

Bonus Question: Do I have a larger concentration of pre-tax or Roth IRAs and retirement plans?

- By having a large concentration of only pre-tax IRAs and retirement plans, you will be subject to required minimum distributions (RMDs) and must start paying taxes on this money at age 73.

- By having a tax-diversified portfolio with some pre-tax and some Roth IRAs, you will have flexibility to draw from both account types in an effort to minimize tax liability.

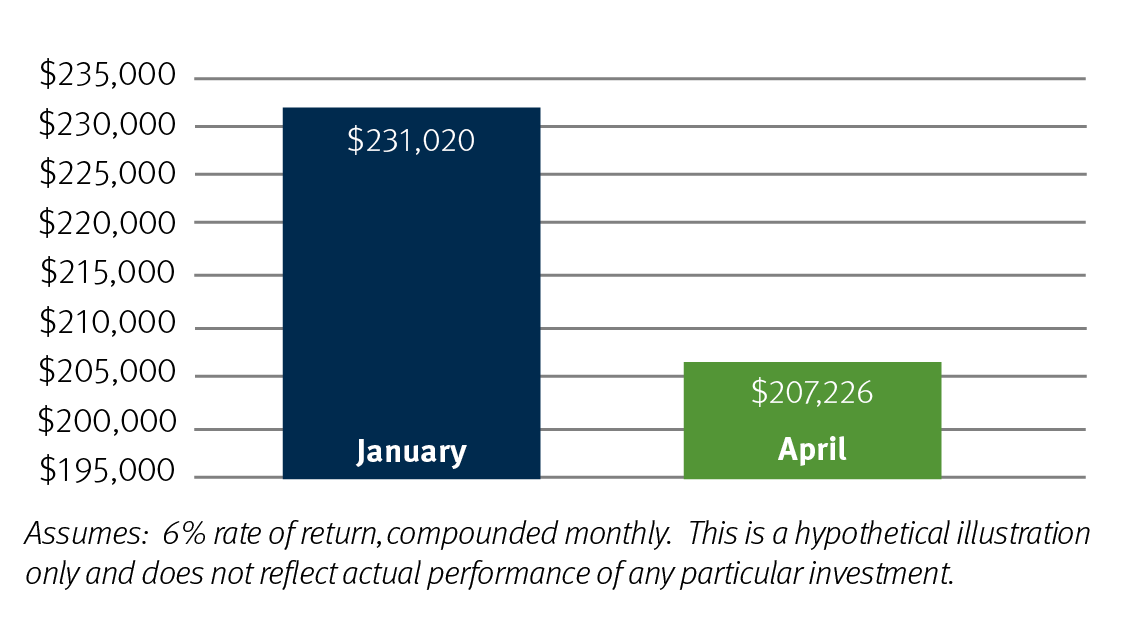

Why contributing early in the year matters

IRA owners can make IRA contributions for 2023 from January 1, 2023, to April 18, 2024, so why does it pay off to contribute early?

Over the course of 20 years, a $6,000 contribution invested in January of each tax year versus in April of the following year can make a significant difference:

As you can see, by waiting just 15 months, the cost could be $23,794. By making IRA contributions earlier in the year, the account’s value will have more time to grow and compound earnings.

This information is for educational purposes only. Stifel does not provide tax advice.

You should consult with your legal and tax advisors regarding your particular situation.

0123.5436556.1