IRA Maximization

Using IRA Distributions to Fund a Life Insurance Policy

Concern

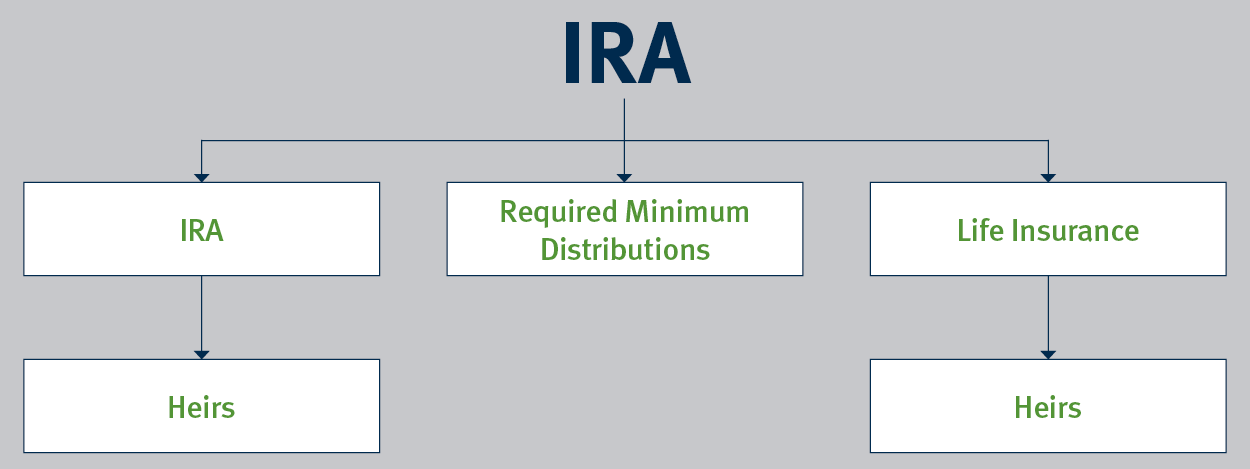

After many years of hard work, you are finally getting ready to retire! Over the years, you contributed diligently to your IRA; however, now that you are approaching retirement, you realize that your retirement income needs have been over funded. At this point, your IRA becomes an asset and you want to leave it to your heirs. This may be challenging, as your heirs would have to deal with income and estate taxes. In addition, once you reach age 73, you are required to take Required Minimum Distributions (RMDs) from your plan, even if you do not need the money. IRA Maximization is a wealth transfer strategy that will allow you to reposition the value of your IRA in a more tax-efficient manner.Solution

When done properly, distributions from your IRA are used to fund a life insurance policy, helping to manage your tax liability and maximize the legacy that passes to your heirs.How It Works

Create an income stream by taking required distributions (or more) from your IRA. You pay income tax on the withdrawals, but then can use the after-tax money to fund a life insurance policy. Your heirs will receive a lump-sum tax-free death benefit upon your death. Any remaining IRA balance passes to your designated beneficiaries and is included in your estate subject to income and estate taxes.Benefits

- Life Insurance can increase the amount of money left for heirs.

- Life Insurance provides an income tax-free death benefit.

- Life Insurance cash values grow tax deferred.

Considerations

- You must pay income tax on the withdrawals as you take them from the qualified plan. Should you take withdrawals greater than your RMDs, you may reduce the value of your qualified plan.

- The strategy might not be suitable if you plan to use IRA money during your lifetime.

- The amount of life insurance protection you qualify for will be subject to medical and financial underwriting requirements and may be more (or less) than the amount applied for.

- The purchase of life insurance has costs and risks associated with it, including the cost of insurance.

- Distributions from the IRA are taxable to the recipient.

- You may want to consider establishing an Irrevocable Life Insurance Trust (ILIT) to hold the life insurance to remove the policy from your taxable estate.

- Income and estate tax laws are subject to change at any time.

Stifel does not provide legal or tax advice. You should consult with your legal and tax advisors regarding your particular situation.

1224.3251628.5