Key Person Life Insurance

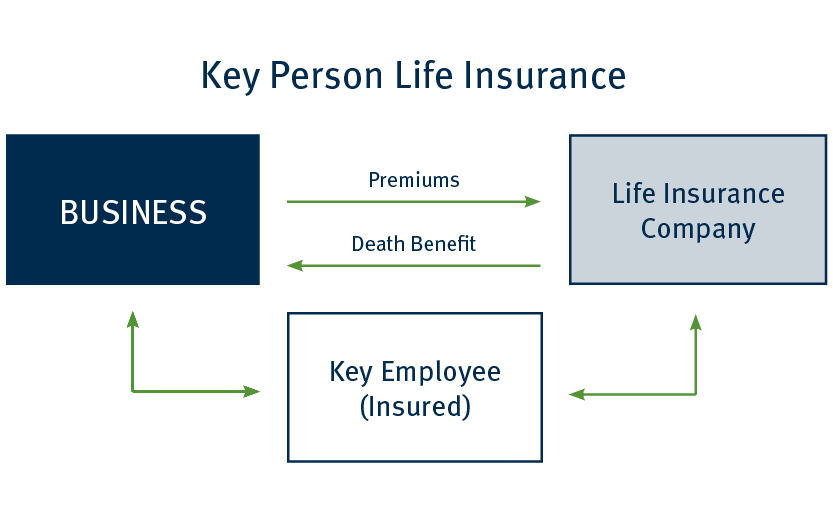

Key person life insurance provides a business with protection against economic loss suffered from the death of a key employee. Key employees are any employee whose death will negatively impact a company by reducing revenue due to lost business and/or increasing expenses by the need to hire and train an adequate replacement. The business owns the life insurance policy, pays the premiums, and is the sole beneficiary. The key employee is the insured. Upon the death of the key employee, the business generally receives the life insurance death benefit free of federal income tax.

Benefits to the Business

- Provides cash to indemnify business for lost sales

- Assures creditors that business is financially sound

- Offers comfort to customers that business will continue operations

- Allows business to recruit and hire a qualified replacement

Tax Considerations

- Death benefit generally received income tax free

- No tax deduction for life insurance premiums

- Potential alternative minimum tax liability for “C” corporations

Factors Making Employee “Key”

- Employee has special knowledge about operations and products/services

- Rival companies would have an advantage if employee was gone

- Employee is the relationship initiator and facilitator

- Cannot meet sales goals without employee

- Business can’t obtain sufficient financial backing without employee

Factors Determining Insurance Amount

- Cost to replace the employee

- Amount employee is worth to the bottom line

- Total economic loss to the business

- Typical formula is five to ten times annual compensation of key employee

IRS CIRCULAR 230 DISCLOSURE: To ensure compliance with the requirements imposed by IRS Circular 230, we inform you that to the extent this communication, including attachments, mentions any federal tax matter, it is not intended or written and cannot be used for the purpose of avoiding Federal Tax penalties. In addition, this communication may not be used by anyone in promoting, marketing, or recommending the transaction or matter addressed herein. Anyone other than the recipient who reads this communication should seek advice based on their particular circumstances from an independent tax advisor. Stifel does not provide legal or tax advice.

0523.3124980.3