Taking Loans From Employer-Sponsored Retirement Plans

Most employer-sponsored retirement plans allow participants to take loans from their accounts. If your plan does allow loans, you can borrow up to 50% of your vested balance or $50,000, whichever is less.

There may also be specific repayment terms. Loan repayments are made with after-tax dollars, and interest is paid back to your account for the length of the loan. Generally, retirement plans give you five years to pay back the loan. However, if you use the loan to buy your first home, you may have up to 30 years to repay it. The IRS suggests loan repayments be paid at least quarterly in equal amounts that include principal and interest. These limits and terms are stated in your plan documents.

On the other hand, taking out a loan may negatively impact your future retirement savings. For instance, some participants will contribute less to their plans while they are focused on paying back their outstanding loan. You may also experience lost earnings on the amount that could have accrued while making such repayments.

If you should decide to leave your current employer, you may have less time to pay off the outstanding loan balance and can potentially incur income taxes and penalties if the loan is not paid off within that specified time period. The IRS considers your entire remaining balance as a taxable withdrawal. Therefore, it will be taxed at both the state and federal levels. If you are under age 59½, you would also owe a 10% early withdrawal penalty.

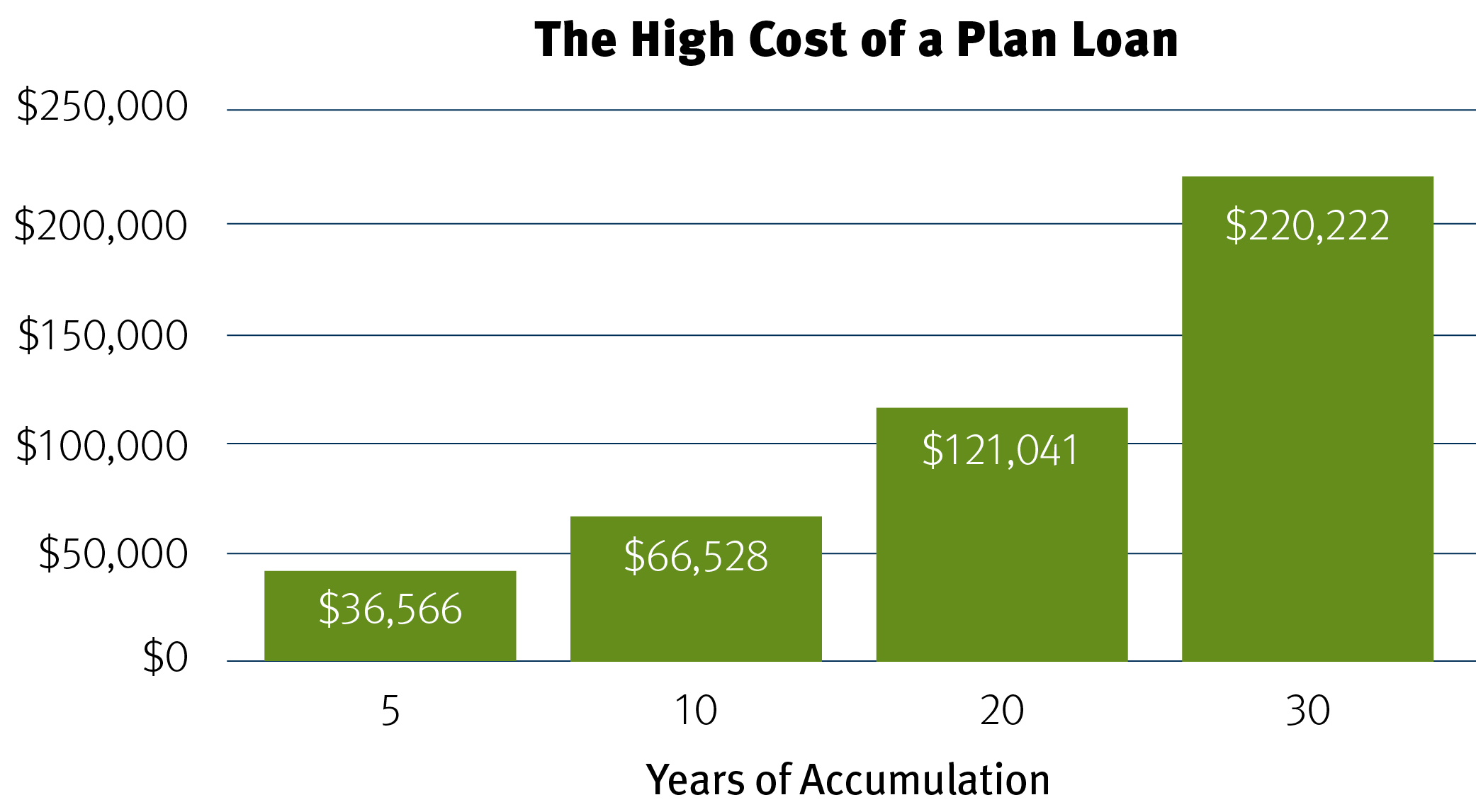

Just look at the savings you would be missing out on if you took out a $30,000 loan, repaid it over five years, while also temporarily halting your contributions (based on a starting balance of $100,000 and $500 pretax contributions each month).

Some questions you should ask yourself before taking a loan:

- Is it for a financial emergency?

- Do I have other financial resources available?

- What are my plan’s loan provisions?

- Will I be able to repay the loan?

- Will I stay at my current employer long enough to repay my loan?

- Will I still be on track for retirement?

Stifel does not provide legal or tax advice. You should consult with your legal and tax advisors regarding your particular situation.

1023.3931637.2